In recent years, fintech and financial inclusion through mobile banking have moved from the periphery of development finance into the center of global economic policy discussions. Mobile-based financial services—once viewed primarily as consumer convenience tools—are now increasingly positioned as core infrastructure for reaching populations excluded from traditional banking systems.

Our analysis suggests that this shift is not driven by technology alone. Instead, it reflects a convergence of regulatory reform, smartphone penetration, and targeted fintech innovation aimed at structurally underserved groups. As governments and international institutions seek scalable solutions to reduce inequality and stimulate inclusive growth, mobile banking has emerged as a pragmatic, data-backed mechanism with measurable impact.

Why this matters is straightforward: access to basic financial services is strongly associated with household resilience, small business formalization, and broader economic participation. The question is no longer whether mobile banking can support financial inclusion, but under what conditions it does so sustainably—and where the limits remain.

The Evolution of Financial Access in a Mobile-First World

Financial exclusion has long been a structural feature of many economies. Traditional banking models rely on physical branches, formal identification, and stable income documentation—requirements that systematically exclude rural populations, informal workers, migrants, and low-income households.

According to World Bank financial inclusion research, digital financial services have reshaped this equation by reducing marginal transaction costs and bypassing physical infrastructure constraints. The rapid expansion of mobile networks across Africa, South Asia, and parts of the Middle East created the foundation for mobile money platforms well before similar adoption in advanced economies.

Our review of historical adoption patterns indicates that mobile banking succeeded where it addressed a concrete gap: safe storage of value and low-cost person-to-person transfers. Over time, these platforms expanded into savings, credit scoring, insurance, and government-to-person payments, embedding themselves into everyday economic activity.

Recent Developments in Mobile Banking–Led Inclusion

The latest phase of mobile banking adoption is characterized by integration rather than experimentation. Regulators in multiple regions have formalized licensing regimes for non-bank financial service providers, while central banks increasingly treat mobile wallets as part of national payment systems.

Based on recent updates from World Bank digital finance initiatives, several trends stand out:

- Mobile wallets are being linked directly to national ID systems.

- Governments are using mobile platforms to distribute social benefits.

- Fintech firms are partnering with traditional banks rather than displacing them.

Importantly, these developments signal institutional acceptance. Mobile banking is no longer operating in regulatory gray zones but is being embedded into formal financial architectures.

Why Mobile Banking Has Become a Policy Priority

From a policy perspective, the significance of mobile banking lies in its multiplier effects. Financial access enables households to smooth consumption, manage risk, and invest in education or microenterprise activity. At scale, these individual effects aggregate into broader economic participation.

Our analysis highlights three key implications:

Societal impact

Mobile banking reduces reliance on cash, improving transaction security and transparency. This is particularly relevant for women and rural populations, where physical access to banks is limited.

Economic implications

For small and medium-sized enterprises, digital financial footprints enable access to credit products previously unavailable through formal channels. This dynamic aligns with themes explored in Malota Studio’s analysis on how MSMEs adapt to digital competition.

Policy relevance

Digital finance supports more efficient fiscal transfers and improves monitoring of public spending, a priority emphasized in multiple IMF financial access assessments.

Data Signals and Adoption Trends Across Regions

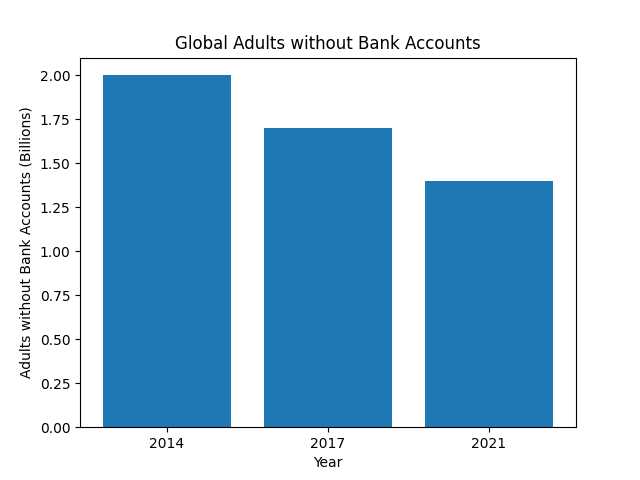

While progress is uneven, the direction of travel is consistent. Global data indicates a steady decline in the unbanked population alongside a rise in mobile account ownership.

Selected Indicators on Mobile Banking and Inclusion

| Indicator | 2014 | 2017 | 2021 |

|---|---|---|---|

| Adults without bank accounts (global) | ~2.0 billion | ~1.7 billion | ~1.4 billion |

| Adults with mobile money accounts | Limited | Moderate growth | Widespread in EMs |

| Government payments delivered digitally | Low | Expanding | Mainstream in several regions |

Source synthesis based on World Bank Global Findex data and institutional reviews.

Regionally, Sub-Saharan Africa remains the most advanced in mobile money usage, while South Asia shows rapid acceleration driven by government-backed digital identity systems. Advanced economies, by contrast, demonstrate slower adoption for inclusion purposes, as legacy banking penetration is already high.

Institutional Perspectives on Digital Financial Inclusion

International organizations broadly converge on the role of fintech as an enabler rather than a standalone solution. The OECD’s digital economy policy work emphasizes that mobile banking outcomes depend heavily on consumer protection, competition policy, and data governance frameworks.

Academic research summarized by institutions such as MIT’s financial inclusion initiatives further underscores that access alone is insufficient. Sustained inclusion requires product design aligned with user behavior, transparent pricing, and financial literacy interventions.

From an industry standpoint, partnerships between telecom operators, fintech startups, and regulated banks are increasingly viewed as best practice, balancing innovation with systemic stability.

Monitoring the Next Phase of Mobile Banking Expansion

Looking ahead, several factors warrant close attention rather than firm prediction.

First, regulatory capacity will shape outcomes. Jurisdictions that align fintech oversight with consumer protection are more likely to see durable inclusion gains. Second, data privacy and cybersecurity risks will grow as mobile platforms accumulate sensitive financial information.

Finally, inclusion metrics themselves are evolving. As highlighted in Malota Studio’s coverage of AI-driven transformation in financial services, the next frontier may involve using alternative data responsibly to expand credit access without reinforcing bias.

Visual & Data Considerations for Editorial Use

The dataset above is suitable for conversion into:

- A time-series chart tracking unbanked population decline

- A regional comparison infographic on mobile money adoption

- A policy impact visualization linking digital payments to fiscal efficiency

All indicators should be presented with neutral labeling and clear source attribution.

Resources

Internal Reading

External References

- World Bank financial inclusion programs

- Global Findex Database

- IMF work on financial access

- OECD digital economy policy analysis

Author Bio

Written by the editorial team of Malota Studio, focusing on data-backed analysis and visual storytelling across science, technology, and public policy topics.