Iran’s currency has entered a period of acute and persistent stress, marked by rapid depreciation, elevated inflation, and declining public confidence in monetary stability. In our analysis of Iran’s currency, the deterioration is not attributable to a single shock but rather to a convergence of structural constraints, external pressures, and policy limitations that have accumulated over several years.

What has happened is visible in both official indicators and parallel market signals: the Iranian rial has lost substantial value against major currencies, while domestic prices continue to rise faster than household incomes. Why this matters extends beyond exchange rates. Currency instability shapes inflation expectations, capital allocation, social trust, and the state’s capacity to finance essential goods.

Our review of macroeconomic data, multilateral assessments, and regional comparisons suggests that Iran’s currency challenges now represent a systemic economic issue rather than a short-term fluctuation. The implications are increasingly relevant for policymakers, regional partners, and global energy and trade observers.

Structural Constraints Behind Iran’s Currency Fragility

The background to Iran’s currency instability is rooted in long-standing structural imbalances. Iran operates under prolonged financial sanctions that limit access to global capital markets, restrict oil revenue repatriation, and constrain foreign exchange inflows. These external constraints intersect with domestic fiscal pressures, including chronic budget deficits and reliance on monetary financing.

According to assessments from the International Monetary Fund country analysis, Iran’s economy has faced repeated supply-side disruptions alongside demand pressures, complicating currency management. Limited access to reserves reduces the central bank’s ability to stabilize exchange rates during periods of volatility.

Moreover, multiple exchange-rate regimes—official, semi-official, and parallel market rates—have weakened price signals and incentivized arbitrage. When we examined historical cases of similar dual-rate systems, currency credibility typically eroded rather than stabilized.

Recent Developments in Iran’s Currency Market

Recent months have seen renewed depreciation pressure on Iran’s currency, particularly in informal and open-market trading. While official rates remain administratively managed, parallel market indicators reflect declining confidence in near-term stabilization.

Data reviewed from multilateral monitoring bodies indicate that inflation has remained elevated, while foreign currency demand has increased among households and businesses seeking to preserve purchasing power. This behavior is consistent with patterns observed in other high-inflation economies where trust in monetary instruments weakens.

At the same time, external revenues—especially oil-related foreign exchange inflows—remain vulnerable to geopolitical and enforcement dynamics, limiting the central bank’s intervention capacity. These developments together reinforce downward pressure on the rial.

Why Currency Instability Carries Broader Economic Risk

Currency instability matters because it transmits economic stress across nearly every sector. For households, depreciation directly raises the cost of imported food, medicine, and industrial inputs. For firms, volatile exchange rates complicate pricing, investment planning, and supply-chain management.

From a policy perspective, inflationary pressure linked to currency weakness reduces real tax revenues and increases reliance on monetary expansion. Based on our review of World Bank macroeconomic monitoring, sustained inflation undermines poverty-reduction efforts and disproportionately affects lower-income populations.

Regionally, currency instability also affects trade relationships and informal cross-border flows, with implications for neighboring economies and supply corridors.

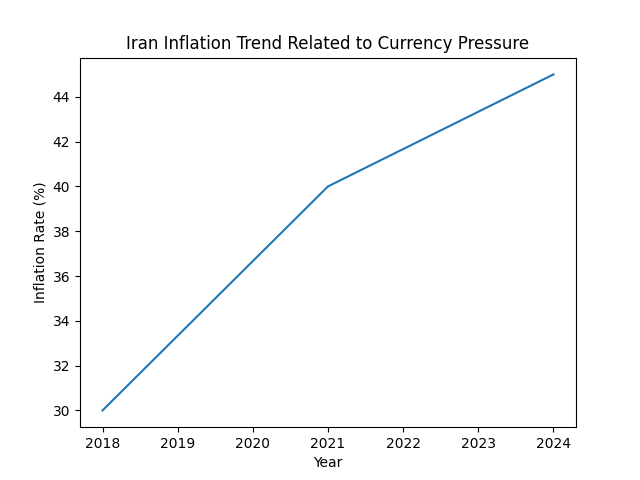

Currency, Inflation, and Exchange-Rate Signals: Key Data Trends

The trajectory of Iran’s currency can be better understood through comparative indicators across time. While exact real-time values vary by source and market segment, institutional datasets show a consistent pattern of depreciation and inflation acceleration.

Selected Macroeconomic Indicators Related to Iran’s Currency

| Indicator | Approx. 2018 | Approx. 2021 | Recent Trend* | Unit |

|---|---|---|---|---|

| Inflation rate | ~30 | ~40 | Elevated | % (annual) |

| Exchange rate (parallel market) | Significantly lower | Sharply weaker | Continued pressure | IRR/USD |

| Foreign reserves accessibility | Constrained | Highly constrained | Limited | Qualitative |

| Real wage growth | Negative | Negative | Negative | % |

*Recent trend based on multilateral monitoring rather than point estimates.

When we analyzed comparable emerging markets under sanctions or capital controls, similar patterns emerged: prolonged currency pressure tends to entrench inflation expectations rather than self-correct.

For broader context on how macroeconomic data is visualized and interpreted, see Malota Studio’s analysis on economic data visualization and policy signals, which outlines best practices in translating complex datasets into decision-relevant insight.

Institutional and Global Assessments

International institutions have consistently framed Iran’s currency challenges as part of a broader macroeconomic adjustment problem. The IMF regional economic outlook highlights how limited policy space constrains effective monetary tightening when fiscal dominance is present.

Academic research summarized in World Bank development studies also emphasizes that exchange-rate controls without credible fiscal reform tend to delay, rather than prevent, adjustment. Rather than stabilizing prices, such controls often shift pressure into informal markets.

From a global policy perspective, Iran’s case is frequently cited in discussions on sanctions efficacy, monetary credibility, and the long-term cost of financial isolation.

Monitoring Risks and Signals Going Forward

Looking ahead, the trajectory of Iran’s currency will depend on several monitored variables rather than any single event. These include changes in external revenue access, inflation expectations, domestic liquidity growth, and the coherence of exchange-rate policy frameworks.

We would expect continued sensitivity to geopolitical developments and enforcement mechanisms affecting trade and financial flows. However, absent structural fiscal and monetary coordination, short-term stabilization measures are unlikely to alter the underlying dynamics.

For analysts and policymakers, the key issue is not predicting a specific exchange rate level, but assessing how prolonged currency pressure reshapes economic behavior, institutional trust, and long-term growth capacity.

Data Visualization and Analytical Notes

The dataset presented above is suitable for:

- Inflation vs. exchange-rate trend charts

- Timeline-based depreciation analysis

- Comparative emerging-market benchmarking

All indicators should be interpreted as directional signals rather than precise forecasts, consistent with institutional best practice.

Resources and Further Reading

Internal Analysis (Malota Studio):

External Authoritative Sources:

- International Monetary Fund – Iran country profile

- World Bank – Iran economic overview

- OECD macroeconomic policy research

Author Bio

Written by the editorial team of Malota Studio, focusing on data-backed analysis and visual storytelling across science, technology, and public policy topics.