Introduction

An effective ESG reporting workflow for enterprises has moved from a compliance exercise to a core business capability. Large organisations are now expected to produce consistent, audit-ready sustainability disclosures across multiple frameworks and jurisdictions. According to the <a href=”https://www.pwc.com/gx/en/services/sustainability/publications/global-investor-survey.html” target=”_blank” rel=”noopener”>PwC Global Investor Survey</a>, over 79% of investors consider ESG risks an important factor in investment decisions, highlighting why structured ESG reporting processes are under executive scrutiny.

In my experience working with enterprise reporting environments, the biggest challenge is not producing a single ESG report—it is building a repeatable, governed system that connects data, teams, and disclosures. This article breaks down how mature organisations design and operationalise their ESG reporting lifecycle, supported by industry data and practical observations.

Business Context and Industry Background

Enterprise ESG reporting now spans finance, operations, risk, IT, and corporate communications. The shift is largely driven by regulatory expansion and investor expectations.

The <a href=”https://www.mckinsey.com/capabilities/sustainability/our-insights/the-esg-premium-new-perspectives-on-value-and-performance” target=”_blank” rel=”noopener”>McKinsey ESG research</a> notes that companies with strong ESG propositions can experience lower cost of capital and improved operational resilience, which has elevated ESG from a reporting task to a strategic function.

In large organisations, the ESG reporting process typically involves:

- Chief Sustainability Officer and ESG teams

- Finance and controllership functions

- Risk and compliance departments

- IT and data engineering teams

- Investor relations and corporate communications

- Internal audit and external assurance providers

The complexity increases further when companies operate across multiple regions with different reporting standards such as ISSB, GRI, TCFD, and regional regulations.

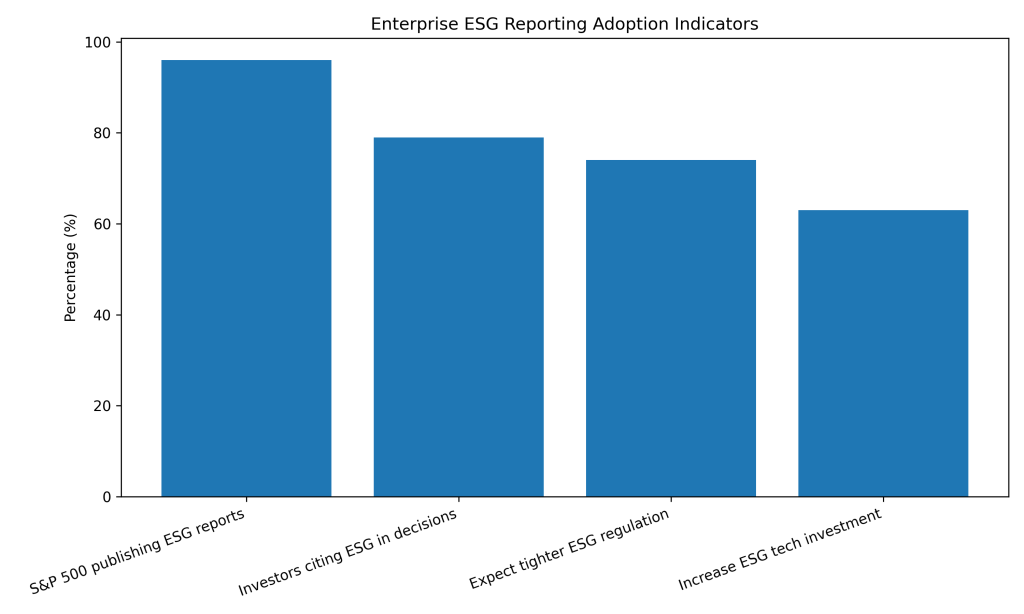

Table: Enterprise ESG Reporting Adoption Indicators

| Metric | Value | Source |

|---|---|---|

| S&P 500 companies publishing ESG reports | 96% | Governance & Accountability Institute (2023) |

| Investors citing ESG in decisions | 79% | PwC Global Investor Survey |

| Companies expecting tighter ESG regulation | 74% | Deloitte Sustainability Action Report |

| Firms planning to increase ESG tech investment | 63% | EY Global Climate Risk Barometer |

Table note: Data compiled from publicly available industry reports (2023–2024).

This data confirms that ESG reporting is now standard practice among large enterprises—but maturity levels still vary significantly.

Key Challenges Companies Face

Fragmented sustainability data collection

One of the most persistent obstacles in the ESG reporting process is data fragmentation. Large enterprises often pull sustainability metrics from dozens of operational systems.

The <a href=”https://www.ey.com/en_gl/assurance/how-the-esg-reporting-landscape-is-changing” target=”_blank” rel=”noopener”>EY Global Climate Risk Barometer</a> highlights that many companies still rely heavily on manual data aggregation, which increases error risk and slows reporting cycles.

In complex organisations, ESG data may originate from:

- Energy management systems

- HR platforms

- Supply chain databases

- Environmental monitoring tools

- Finance systems

Without strong data architecture, reconciliation becomes resource-intensive.

Unclear ESG governance workflow

Many enterprises struggle to define ownership across the ESG governance workflow. Sustainability teams often lead reporting, but underlying data sits with operational units.

This creates common issues:

- Delayed data validation

- Inconsistent definitions

- Weak audit trails

- Limited executive visibility

In global organisations, governance gaps can add several weeks to the ESG reporting lifecycle.

Rapidly evolving disclosure requirements

Regulatory pressure continues to intensify. According to Deloitte, three-quarters of executives expect ESG regulation to become significantly stricter in the near term.

Enterprises must now manage:

- Multiple reporting frameworks

- Jurisdiction-specific rules

- Scope expansions (especially Scope 3 emissions)

- Assurance readiness requirements

This regulatory volatility makes static workflows quickly obsolete.

Limited integration between ESG and financial reporting

Despite progress, many organisations still treat ESG and financial reporting as separate processes. This separation creates challenges when stakeholders expect integrated narratives.

Common enterprise symptoms include:

- Misaligned reporting timelines

- Duplicate controls

- Inconsistent risk disclosures

- Manual reconciliation between finance and sustainability metrics

Best Practices and Professional Approaches

Establish a centralised ESG data architecture

Leading enterprises are investing in unified sustainability data platforms. A centralised model reduces manual work and improves traceability.

Typical maturity indicators include:

- Automated data ingestion from operational systems

- Standardised metric definitions

- Built-in validation rules

- Role-based access controls

Organisations that implement structured data pipelines often report material reductions in reporting cycle time, according to multiple consulting benchmarks.

Define clear cross-functional ownership

Mature ESG reporting workflow for enterprises depends on explicit accountability. High-performing companies typically formalise:

- Data owners at business unit level

- ESG methodology owners

- Finance validation checkpoints

- Executive review gates

This governance clarity reduces last-minute escalations and improves audit readiness.

Align ESG reporting lifecycle with financial calendar

Enterprises that synchronise ESG and financial reporting tend to achieve stronger credibility with investors.

Common alignment practices include:

- Quarterly ESG data reviews

- Pre-close sustainability checks

- Integrated risk committee oversight

- Shared materiality assessments

In large public companies, ESG reporting cycles increasingly mirror financial reporting discipline.

Invest in automation and workflow tooling

Automation is becoming a major differentiator. According to EY analysis, companies increasing ESG technology investment expect improved data confidence and faster reporting.

Typical automation use cases:

- Emissions calculations

- Supplier data ingestion

- Control testing

- Disclosure generation

- Dashboard refresh cycles

Enterprises deploying workflow automation often reduce manual intervention significantly, particularly in Scope 1 and Scope 2 reporting.

Data, Reporting, and Documentation Perspective

From an enterprise reporting standpoint, ESG outputs must serve multiple audiences simultaneously: regulators, investors, boards, and internal leadership.

A mature ESG reporting process typically includes:

Structured reporting cadence

- Monthly operational ESG dashboards

- Quarterly executive ESG reviews

- Annual external sustainability reports

- Ongoing regulatory submissions

Governed documentation layers

- Methodology documentation

- Data dictionaries

- Control matrices

- Audit evidence repositories

Typical enterprise KPI ranges

While metrics vary by industry, many organisations track:

- Emissions intensity (year-over-year reduction targets)

- Workforce diversity ratios

- Safety incident rates

- Supplier ESG coverage percentages

- Climate risk exposure metrics

The key is not just measurement but decision usability. Executives increasingly expect ESG dashboards to support capital allocation, risk management, and strategic planning.

Common Mistakes to Avoid

Treating ESG reporting as a once-a-year exercise

Enterprises that only mobilise teams during annual reporting often face compressed timelines and quality issues. This approach frequently results in last-minute data gaps and higher assurance costs.

Over-reliance on manual spreadsheets

Manual workflows may work at small scale but break down quickly in global organisations. Spreadsheet-heavy processes are associated with higher error rates and weaker audit trails.

Weak executive sponsorship

Without strong C-suite involvement, ESG initiatives often stall at the data collection stage. Organisations with active executive oversight typically achieve faster ESG maturity.

Ignoring data lineage and auditability

Many companies focus on disclosure formatting but neglect data traceability. This becomes a major risk as external assurance requirements expand.

Underestimating Scope 3 complexity

Scope 3 emissions remain one of the largest reporting challenges. Enterprises that delay supplier engagement often face significant data gaps and estimation uncertainty.

Conclusion

For large organisations, building a robust ESG reporting workflow for enterprises is no longer optional—it is a foundational capability for regulatory readiness, investor confidence, and strategic decision-making. With 96% of S&P 500 companies already publishing ESG reports, the competitive question is no longer whether to report, but how efficiently and reliably enterprises can operationalise the ESG reporting lifecycle.

Enterprises that invest early in governance clarity, data architecture, and cross-functional alignment are consistently better positioned to meet the next wave of sustainability disclosure demands.

References and Data Sources

- PwC — Global Investor Survey

https://www.pwc.com/gx/en/services/sustainability/publications/global-investor-survey.html - McKinsey — The ESG premium: New perspectives on value and performance

https://www.mckinsey.com/capabilities/sustainability/our-insights/the-esg-premium-new-perspectives-on-value-and-performance - EY — Global Climate Risk Barometer

https://www.ey.com/en_gl/assurance/how-the-esg-reporting-landscape-is-changing - Governance & Accountability Institute — S&P 500 ESG Reporting Trends

https://www.ga-institute.com - Deloitte — Sustainability Action Report

https://www2.deloitte.com