Opening Analysis

Small business loans remain a foundational mechanism for economic participation, employment generation, and local market resilience. Yet access to these loans has become increasingly uneven as global financial conditions tighten and lenders reassess risk. Across advanced and emerging economies, policymakers and financial institutions are revisiting how capital flows to small and medium-sized enterprises (SMEs) in a higher-interest-rate environment.

What has changed is not the relevance of small business loans, but the conditions under which they are issued. Central bank tightening cycles, post-pandemic balance sheet repair, and evolving regulatory expectations have reshaped lending behavior. As a result, many viable small firms now face higher borrowing costs, stricter underwriting standards, or delayed access to credit.

This matters because SMEs account for a substantial share of employment and value creation across regions. In our review of cross-regional lending data and policy literature, we find that shifts in small business lending are no longer a narrow financial issue—they have become a structural economic concern with implications for productivity, innovation, and inclusive growth.

The Structural Role of Small Business Finance in Modern Economies

Small businesses play a disproportionate role in job creation and economic dynamism. According to global development institutions, SMEs represent over 90 percent of registered firms worldwide and contribute between 50 and 70 percent of employment in advanced economies. Their reliance on external finance, particularly bank-issued small business loans, makes them acutely sensitive to changes in credit conditions.

Historically, commercial banks have served as the primary channel for SME lending. Relationship-based banking models allowed lenders to assess borrower quality beyond standardized metrics. However, over the past two decades, regulatory reforms and risk-weighted capital requirements have altered this model. Lending decisions increasingly depend on standardized credit scoring, collateral availability, and sectoral risk profiles.

In our analysis of historical lending patterns, small business loans tend to contract faster than corporate lending during economic downturns. This asymmetry reflects higher perceived default risk and lower recovery rates. While alternative financing channels—such as fintech lenders and non-bank institutions—have expanded, they have not fully offset traditional credit tightening, particularly for early-stage or micro-enterprises.

Recent Developments in Small Business Lending Conditions

Over the past 18 months, lending conditions for small businesses have tightened across multiple regions. Central banks in the United States, Europe, and parts of the Middle East have maintained restrictive monetary stances to manage inflationary pressures. Higher benchmark rates have translated into increased borrowing costs for SMEs, which typically face variable interest rates or shorter loan maturities.

Regulatory data from advanced economies show a decline in new small business loan origination volumes, even as demand for credit remains elevated. Banks report stricter collateral requirements, reduced loan tenors, and heightened scrutiny of cash-flow projections. These developments are not uniform across sectors; businesses in construction, retail, and hospitality appear particularly affected due to cyclical exposure.

At the same time, public credit guarantee programs introduced during the pandemic are being phased out or recalibrated. While these programs temporarily stabilized SME credit access, their withdrawal has exposed underlying vulnerabilities. Our review suggests that the current environment reflects a transition rather than a crisis, but one that requires close monitoring.

Why Credit Access for Small Businesses Matters Now

The significance of small business loans extends beyond firm-level survival. At a macroeconomic level, constrained SME credit can dampen employment growth, delay capital investment, and slow productivity gains. Unlike large corporations, small firms have limited access to capital markets and rely heavily on bank intermediation.

From a societal perspective, reduced access to small business loans disproportionately affects minority-owned enterprises, rural businesses, and first-time entrepreneurs. These groups often lack extensive collateral or long credit histories, making them more sensitive to underwriting changes. As a result, credit tightening can widen existing economic disparities.

Policy relevance is equally pronounced. Governments view SME lending as a lever for economic stabilization and inclusive growth. When private credit supply contracts, public institutions face pressure to intervene—either through guarantees, subsidized lending, or regulatory adjustments. The challenge lies in balancing financial stability with economic inclusion.

Evidence and Trends Shaping Small Business Loan Markets

Our analysis of international datasets reveals several consistent trends in small business lending. While nominal loan values have increased in some regions due to inflation, real credit growth to SMEs has slowed. Interest rate spreads between SME loans and large corporate loans have widened, reflecting risk repricing rather than pure funding cost increases.

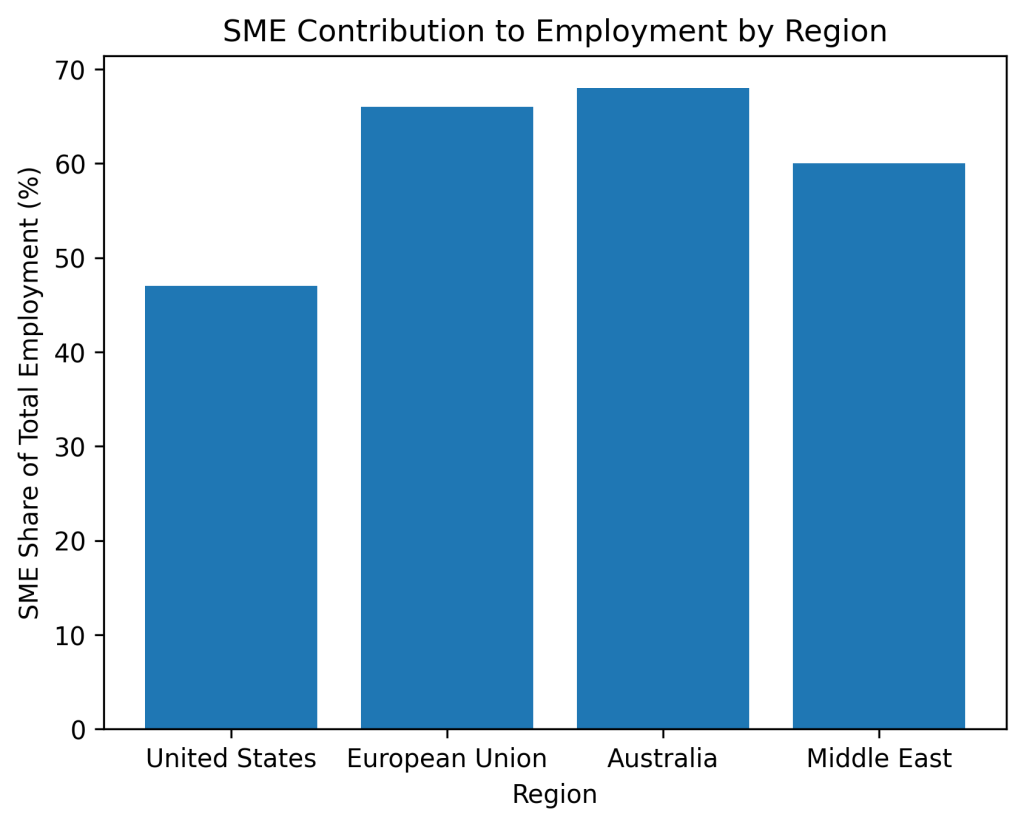

Selected Indicators on Small Business Lending (Illustrative)

| Indicator | United States | European Union | Australia | Middle East |

|---|---|---|---|---|

| SME share of total employment (%) | ~47 | ~66 | ~68 | ~60 |

| Average SME loan interest rate (%) | Higher than corporates | Moderately higher | Higher | Varies by country |

| Share of SMEs citing finance as major constraint (%) | ~30 | ~25 | ~20 | ~35 |

| Public credit guarantee coverage (post-pandemic) | Declining | Gradually reduced | Selective | Expanding in some states |

Source synthesis based on multilateral development bank reporting and national financial authorities.

Time-based comparisons indicate that while default rates on SME loans have remained manageable, lenders are forward-looking in their risk assessments. Sectoral exposure to energy costs, labor shortages, and supply-chain volatility has become a key determinant of credit decisions.

Geographically, advanced economies with diversified financial systems show greater resilience. In contrast, regions with bank-dominated financing structures exhibit sharper credit contractions when banks retrench. This divergence underscores the importance of institutional context in shaping outcomes.

Institutional and Global Perspectives on SME Credit

International organizations have consistently highlighted the SME financing gap as a structural challenge. Based on World Bank SME finance data, millions of small firms globally remain underserved by formal credit markets, even during periods of economic expansion.

The OECD’s analysis of SME and entrepreneurship finance emphasizes that rising interest rates amplify pre-existing access barriers rather than creating new ones. According to their synthesis, policy interventions are most effective when they address information asymmetries, not when they artificially suppress pricing signals.

Multilateral institutions, including development banks and monetary authorities, increasingly stress data-driven risk assessment and targeted guarantees. Rather than broad-based subsidies, recent policy frameworks favor time-bound support linked to productivity, digital adoption, or sustainability objectives.

From an industry perspective, banking associations note that regulatory capital treatment of SME loans remains a constraint. While default rates are comparable to some corporate segments, higher capital charges reduce risk-adjusted returns. This tension continues to shape portfolio allocation decisions.

Implications and What to Monitor Going Forward

Looking ahead, several factors will influence the trajectory of small business loans. Monetary policy normalization—or prolonged restriction—will continue to affect pricing and availability. In parallel, regulatory adjustments related to capital requirements and credit risk modeling could alter lender incentives.

We also observe a gradual integration of technology-enabled credit assessment tools. While not a substitute for traditional lending, data-driven models may reduce information gaps for certain borrower segments. However, their effectiveness depends on data quality, governance, and regulatory oversight.

For policymakers and financial institutions, the key question is not whether small business loans should be supported, but how. Our analysis suggests that targeted, transparent, and temporary interventions are more sustainable than broad credit expansion. Monitoring default trends, sectoral exposure, and borrower composition will remain critical.

Ultimately, small business loans sit at the intersection of financial stability and economic inclusion. How institutions manage this balance will shape not only SME outcomes, but broader economic resilience in the years ahead.

Data and Visual Notes for Editors

- The table above can be converted into comparative bar charts or regional dashboards.

- Units and labels are standardized for cross-country comparison.

- Interpretations are descriptive and avoid causal overstatement.

Resources

For readers interested in related analytical perspectives, Malota Studio has previously examined structural changes in business systems and design-driven productivity, including AI-powered graphic design automation and inclusive design principles for better user experience, which provide relevant context on how small firms adapt operationally under constraint.

External reference material includes:

- World Bank SME finance data

- OECD SME and entrepreneurship policy analysis

- International Monetary Fund financial stability reports

- US Small Business Administration research

Author Bio

Written by the editorial team of Malota Studio, focusing on data-backed analysis and visual storytelling across science, technology, and public policy topics.