Introduction

Energy transition reporting for companies has rapidly moved from a voluntary sustainability exercise to a core enterprise discipline tied to risk management, capital access, and regulatory compliance. According to the International Energy Agency, achieving global net-zero emissions by 2050 requires annual clean energy investment to exceed USD 4 trillion by 2030, underscoring the scale of transformation expected from corporates (https://www.iea.org/reports/net-zero-by-2050).

For enterprise leaders, the pressure is twofold: demonstrate credible decarbonization progress while maintaining financial and operational performance. Investors, regulators, and customers increasingly expect transparent, data-backed climate transition reporting that links strategy to measurable outcomes.

In this article, we examine how large organisations approach energy transition disclosure, the operational challenges they face, and the reporting practices that distinguish mature programs.

Business Context and Industry Background

Across sectors—from heavy industry to SaaS platforms—energy transition is now embedded in corporate strategy. Large enterprises typically integrate corporate energy transition strategy into enterprise risk management, capital planning, and product roadmaps.

Several forces are driving this shift:

- Regulatory expansion of climate disclosures (for example, ISSB and regional mandates)

- Investor demand for comparable emissions and transition data

- Customer procurement requirements tied to Scope 3 emissions

- Rising internal carbon pricing programs

A 2023 global survey by CDP found that over 18,700 companies disclosed environmental data through its platform, representing more than half of global market capitalization (https://www.cdp.net/en/articles/media/companies-worth-half-of-global-market-capitalization-disclose-environmental-data-through-cdp). This level of participation signals that energy transition disclosure is becoming standard practice rather than a niche ESG activity.

Within enterprise environments, the responsibility is typically shared across:

- Sustainability and ESG teams

- Finance and investor relations

- Operations and facilities

- IT and data teams

- Risk and compliance functions

- Executive leadership and boards

The complexity of coordinating these stakeholders is one reason many organisations struggle to produce coherent decarbonization reporting.

Key Challenges Companies Face

Fragmented emissions and energy data

Large enterprises often operate across multiple regions, business units, and legacy systems. As a result, energy and emissions data frequently reside in disconnected platforms.

The Task Force on Climate-related Financial Disclosures (TCFD) status reports have repeatedly shown that data quality and availability remain among the top barriers to effective climate reporting (https://www.fsb-tcfd.org/publications/). In practice, many enterprises still rely on manual consolidation processes that introduce error risk and reporting delays.

Scope three measurement complexity

For many companies, Scope 3 emissions represent the majority of their carbon footprint. The World Resources Institute notes that Scope 3 emissions often account for more than 70% of total emissions in sectors such as technology and retail (https://www.wri.org/insights/scope-3-emissions-calculation-guidance).

However, collecting supplier and value-chain data at scale remains operationally difficult. Procurement teams, suppliers, and sustainability functions must align on methodologies, which can slow climate transition reporting cycles.

Regulatory and framework convergence pressure

Enterprises now face overlapping requirements from frameworks such as ISSB, TCFD, and regional regulations. While convergence is improving, reporting teams still manage multiple mapping exercises.

This creates measurable overhead. Large corporates frequently report that ESG reporting programs require cross-functional input from more than ten internal teams, increasing coordination costs and review timelines.

Linking strategy to financial impact

Investors increasingly expect companies to quantify the financial implications of their transition plans. Yet many organisations still present decarbonization narratives without clear capital allocation or ROI metrics.

This gap weakens credibility. According to research from the Transition Pathway Initiative, only a minority of high-emitting companies fully align capital expenditure plans with their stated climate targets.

Best Practices and Professional Approaches

Establish an enterprise-wide transition governance model

Mature organisations formalise governance early. This typically includes:

- Board-level oversight of climate strategy

- Executive steering committees

- Clearly defined data ownership across business units

Companies with formal climate governance structures are significantly more likely to publish decision-useful disclosures, according to multiple CDP analyses.

In practice, leading enterprises review transition progress quarterly and integrate it into enterprise risk dashboards.

Build a centralised energy and emissions data architecture

High-performing organisations invest in integrated data pipelines rather than spreadsheet-based workflows. Typical enterprise approaches include:

- Automated energy data ingestion from facilities

- Standardised emissions calculation engines

- Audit-ready data trails

- Integration with ERP and financial systems

Implementation timelines vary, but large companies often require 12–24 months to fully operationalise enterprise-grade carbon data platforms.

The payoff is measurable: organisations with automated data systems report materially faster reporting cycles and fewer restatements.

Align disclosures with recognised frameworks

To improve credibility and comparability, enterprises increasingly align decarbonization reporting with globally recognised frameworks such as ISSB and TCFD.

Common alignment practices include:

- Scenario analysis using climate pathways

- Science-based targets validation

- Capital expenditure mapping to transition plans

- Consistent KPI definitions across reports

According to the IFRS Foundation, more than 20 jurisdictions are moving toward ISSB-based reporting, making alignment a forward-looking strategic decision (https://www.ifrs.org/groups/international-sustainability-standards-board/).

Embed transition metrics into operational KPIs

Leading companies avoid treating energy transition as a standalone ESG exercise. Instead, they embed metrics into operational and financial management systems.

Typical enterprise KPIs include:

- Energy intensity per unit of output

- Renewable electricity share

- Scope 1 and Scope 2 reduction trajectory

- Internal carbon price levels

When these metrics appear in executive scorecards, organisations tend to show more consistent year-over-year progress.

Data, Reporting, and Documentation Perspective

From a reporting standpoint, the most effective enterprises treat energy transition data as decision infrastructure rather than a compliance artifact.

Common enterprise reporting patterns include:

- Monthly internal energy dashboards

- Quarterly executive climate reviews

- Annual integrated sustainability reports

- Scenario modelling updates every 12–18 months

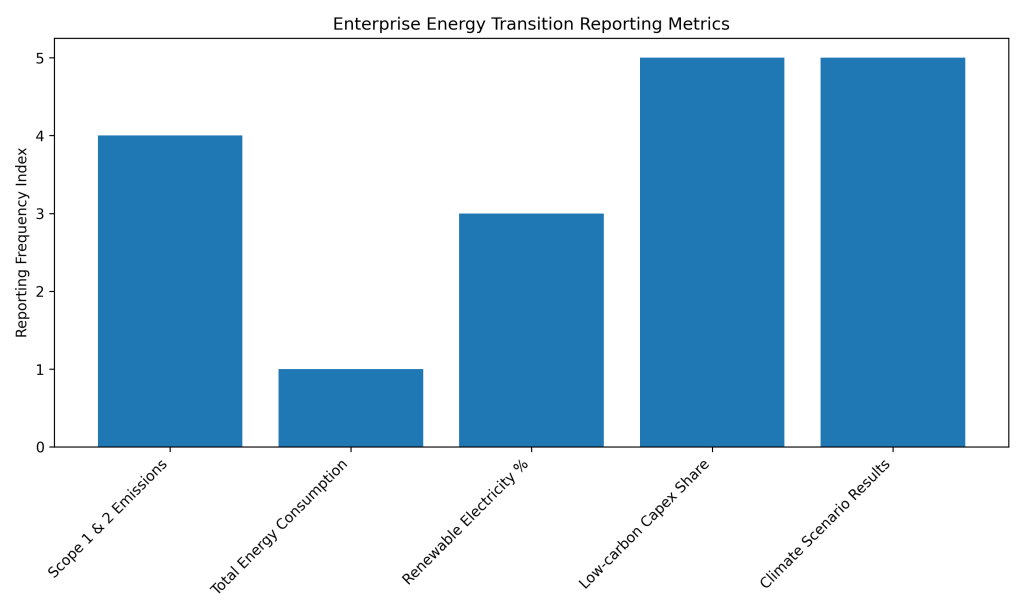

The table below summarises typical enterprise energy transition metrics and reporting frequencies.

Table: Common Enterprise Energy Transition Reporting Metrics

Source: Based on CDP guidance, TCFD recommendations, and IEA reporting practices

| Metric Category | Typical KPI | Common Reporting Frequency | Primary Stakeholders |

|---|---|---|---|

| Emissions | Scope 1 & 2 total emissions | Quarterly internal, annual public | ESG, Finance, Board |

| Energy | Total energy consumption | Monthly internal | Operations, Facilities |

| Renewables | % renewable electricity | Quarterly | Sustainability, Procurement |

| Financial | Low-carbon capex share | Annual | Finance, Investors |

| Risk | Climate scenario stress results | Annual or biannual | Risk, Strategy |

In mature organisations, data governance is tightly controlled. Audit trails, methodology documentation, and version control are standard practice, particularly for companies operating under emerging climate disclosure regulations.

Common Mistakes to Avoid

Treating reporting as a compliance-only exercise

When energy transition reporting is handled purely as a regulatory task, companies often miss strategic insights. This typically results in fragmented initiatives and slower emissions reductions.

Enterprises that fail to integrate reporting into strategy frequently experience multi-year delays in achieving stated targets.

Overreliance on manual data processes

Spreadsheet-heavy workflows increase the risk of calculation errors and audit findings. In large organisations, even small error rates can materially affect reported emissions.

Several ESG assurance providers report that data quality issues remain one of the most common causes of reporting restatements.

Weak cross-functional ownership

If sustainability teams operate in isolation, data gaps and inconsistencies quickly emerge. Procurement, operations, and finance must all contribute.

Enterprises with unclear ownership often see reporting cycles extend by several weeks each year due to reconciliation issues.

Lack of forward-looking transition metrics

Some companies still focus primarily on historical emissions without presenting credible forward pathways. Investors increasingly view this as insufficient.

The consequence is tangible: companies with weak transition narratives may face higher cost of capital or reduced ESG index inclusion.

Conclusion

For large organisations, energy transition reporting for companies is no longer optional—it is a core component of enterprise risk management, investor communication, and long-term value creation. As disclosure expectations continue to converge globally, companies that invest in strong data architecture, governance, and strategy alignment will be better positioned to demonstrate credible progress.

The direction of travel is clear: with thousands of companies already disclosing through platforms like CDP and regulatory requirements expanding worldwide, enterprise-grade climate transition reporting is becoming standard operating practice. Organisations that treat it as strategic infrastructure—rather than a yearly reporting exercise—will move faster and communicate more effectively in the low-carbon transition.

References and Further Reading

- International Energy Agency — Net Zero by 2050: https://www.iea.org/reports/net-zero-by-2050

- CDP Global Disclosure Data: https://www.cdp.net/en/articles/media/companies-worth-half-of-global-market-capitalization-disclose-environmental-data-through-cdp

- World Resources Institute — Scope 3 Guidance: https://www.wri.org/insights/scope-3-emissions-calculation-guidance

- IFRS Foundation — ISSB Standards: https://www.ifrs.org/groups/international-sustainability-standards-board/

- Task Force on Climate-related Financial Disclosures: https://www.fsb-tcfd.org/publications/